Since 2016, China's overall fast-moving consumer goods can be described with one keyword: slowdown. At present, the development of the entire retail industry in China accounts for a large proportion of the total GDP. It is unrealistic for the retail industry to maintain the same growth rate of 20% to 30% each year. On the other hand, China’s urbanization rate has also shown slow development after exceeding 50%. The competition situation faced by offline retailers is even more severe. In such a macro-environment, as a brand merchant, it is more necessary for retailers to understand the needs of consumers, comply with changes in consumer behavior, and continue to innovate.

Under the pressure of online retail sales, the sales of small- and medium-sized retail businesses have shown a good growth, mainly due to the fact that there are smaller convenience stores and small supermarkets in modern channels and some professional channels like cosmetics. Maternal and child channels. In terms of the growth rate of opening stores, the growth rate of mother-and-baby stores reached 13%, cosmetics stores, convenience stores and small supermarkets grew by about 10%, and the number of stores opened in hypermarkets grew by only 5%.

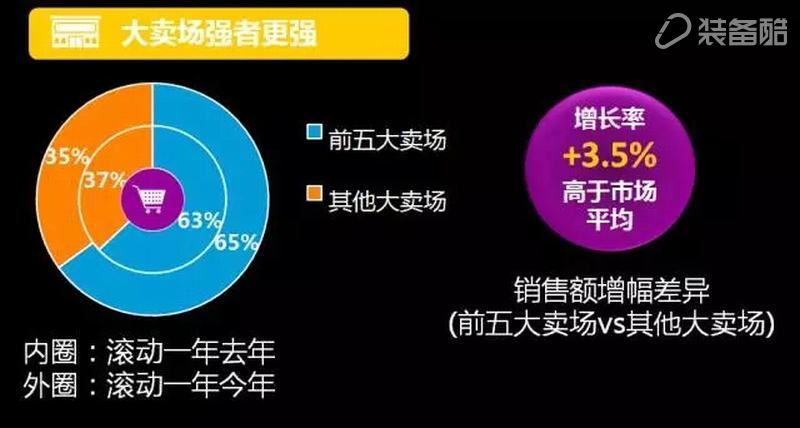

Despite the slowdown in overall channel sales growth in hypermarkets, industry concentration has increased. In the past year, the market-leading Top5 retailers expanded their market share through capital operations such as mergers and acquisitions and equity participation during the market downturn, and their growth rate was 3.5% higher than the market average. It can be seen that leading retailers have higher resistance to industry recession in the face of slowing economic growth.

The impact of cross-border and subdivision of small-scale businesses has promoted the development of overall retail sales. The concept of a professional format-category center stimulated the emergence of more professional category stores. In China, more and more professional category centers are being established in hypermarkets. On the other hand, retailers are not limited to the original format of stores and stores. They also seize the flow of customer spending through cross-border store innovations, including the addition of coffee in convenience stores. The catering part forms an interactive exchange. There will be more and more business operations in the future.

It can be said that the change in China's entire retail channel is adjusted with the overall preference of the middle class. In today's richer material life, the demands of the middle class are more diversified and there are more considerations for consumption. They are looking for convenience and attention to health. They are also willing to pay for quality.

According to the Nielsen data, regular large-scale purchases in the first-tier cities have become the main shopping purpose. In contrast, the main shopping purpose of the fourth-tier cities is still the daily home replenishment. Regular large-scale purchases mean less frequent visits and more purchases in a single purchase. First-tier cities have higher economic income and faster pace of life than consumers in four-tier cities, and they also have more significant features of middle-class consumption. In the past five years, the frequency of visits by shoppers across the country has decreased by 19% in store channels. The average monthly consumption of hypermarkets or department stores has been greatly reduced compared to convenience stores and online shopping.

Consumer demand for convenience is very important. For now, consumer demand for convenience is mainly reflected in:

Savings on shopping time: Whether it's going to stores or online shopping, they all want to spend less time.

The convenience of shopping decisions: Consumers want more and better help to simplify the shopping decision process. Comparison of online products, better display of products through the line, more accurate and optimized selection.

One-stop consumption: Consumer demand for physical retailing has shifted from simple shopping needs to shopping, dining, entertainment, leisure, and friends.

Satisfy the shopping needs based on life situations and scenes: The consumer life forms are increasingly diversified, and the consumer needs based on different life situations and commercial circles also produce significant differences.

Contrary to the ever-increasing consumer demand for convenience, in the retail market, small or fast channels are growing faster and faster, and online shopping is developing particularly rapidly.

In the factors that drive online shopping, the proportion of price factors is declining. Convenience factors include the convenience of selection and comparison, and the proportion of home delivery is constantly increasing. This has also led us to see that e-commerce is paying more and more attention to its own logistics construction, and the delivery speed is constantly challenging the limits.

With the increasing cost of new traffic, maintaining and digging existing customers to provide convenience for their repeated purchases is a cheaper direction for retailers. The promotion of convenience is of great significance to customers in the long term.

The number of stores in China’s convenience stores has doubled in the past five years. However, compared to the developed regions in the world, for example, a convenience store in Japan covers 2,350 people, Taiwan covers about 2,000 people, and Guangzhou and Shanghai cover about 5,000. Our store coverage density still has room for improvement. In the future, with the advancement of urbanization, the steady increase in residents' income and the rapid development of convenience stores will still be possible.

Convenience store development and convenient services make convenience stores a one-stop lifestyle service platform for consumers. At the same time, due to convenience, consumers are also more willing to pay high premiums for the sale of goods. However, how to choose the right products to different channels is still an important issue. Some of the promotional methods in hypermarkets are not suitable for convenience stores. Therefore, for retailers and manufacturers, how to seize the trend of convenience store development needs Note the following points:

1. The commodity structure of convenience stores is becoming more and more high-end, such as packaged water, and the mainstream price in the supermarket channels of supermarkets is 1-2 yuan, while in convenience stores it is 3-4 yuan.

2. Rich fresh food, which is an important factor in forming differentiated competitive advantages for convenience stores and encouraging customers to visit high frequencies.

3, the replacement of new products in the convenience store channel is very fast, the replacement rate of more than 18% per year, compared with the replacement rate in the hypermarket is only about 5%, therefore, convenience stores need to replace the updated goods to meet the young The guests like to taste new requirements.

In addition, from the point of view of form, unlike the supermarket store customers prefer to directly cut prices, convenience store customers have higher acceptance of the membership price. Therefore, for manufacturers and retailers, how to use the membership incentive mechanism to promote the stickiness of member consumption, and at the same time use the pos data generated by the membership consumption, to tap consumer behavior, and develop targeted member incentive mechanisms is to grasp the growth opportunities of convenience store channels The important part.

At the same time, for different consumer commerce circles, retailers and manufacturers need to consider possible application scenarios of consumers and related consumption opportunities, and then provide corresponding products and services. For example, whether a convenience store can never sell a whole box of large packaging products, it also needs to combine the surrounding business districts. If there is consumer demand, how to conveniently implement closed-loop consumption to meet such consumer demand, this requires thinking about the design shopping process from the shopper's point of view.

Based on the increase in consumer demand for one-stop shopping, the transition of the hypermarkets and the main form of the new stores are all based on shopping malls. The shopping mall is younger than the traditional department store. In addition to the simple shopping needs, the young customers' daily consumption also has a richer demand for more diverse life. According to the Nielsen study, 73% of the consumer groups go to the shopping center to eat, and the shopping purpose is only second. And from the changes in recent years, a large part of consumers go to shopping centers for leisure purposes.

In addition, there are significant differences in the consumption patterns of shopping malls of different age groups. Compared to 90 consumers, they are more concerned with the performance of the entertainment industry; and for the 70s and 80s consumers, they may have more attention to children's performance. For retailers and manufacturers, this means that your customer base and their consumption characteristics determine your business mix.

How to apply high-frequency and low-frequency formats, synergies between high-permeability and low-permeability formats, and complementary formats are issues that every retailer and producer must consider.

Sources of this article | Nelson Market Research Pictures 丨 Network

Patient Lift,Medical Patient Lift Hoist,Electric Patient Lift Hoist,Medical Transfer Patient Lift

Jiangmen Jia Mei Medical Products Co.,Ltd. , https://www.jmmedicalsupplier.com